Build and Interpret a Univariate Linear Regression Model

You now understand the three main concepts which are required to build linear regression models: correlation, linearity, and hypothesis testing.

In this chapter, we will apply these concepts to build linear models between variables!

The advertising dataset contains 200 samples with amounts spent on three different media channels: newspaper, radio, and TV. The sales variable is the outcome. Our goal is to understand how spending amounts on each one of these channels influence sales. We start with univariate regression, building linear models between the target variable sales and one input variable at a time. This will allow us to analyze the results in detail, and learn which media is the most efficient to increase sales.

By the end of this chapter, you will be able to:

Build a regression model (between sales and its most correlated media variable).

Interpret the results of the regression using R-squared, p-values of the coefficients, and the t-statistic.

Let's get to work!

The Dataset

This advertising dataset is a classic one in statistical learning. It is analyzed in an excellent book called Introduction to Statistical Learning by James, Witten, Hastie, and Tibshirani, available online for free.

The dataset consists of 200 samples with four variables:

Advertising budgets for newspaper, TV, and radio (the predictors)

Sales (the outcome)

TV Radio Newspaper Sales

0 230.1 37.8 69.2 22.1

1 44.5 39.3 45.1 10.4

2 17.2 45.9 69.3 9.3

3 151.5 41.3 58.5 18.5

4 180.8 10.8 58.4 12.9Visualization

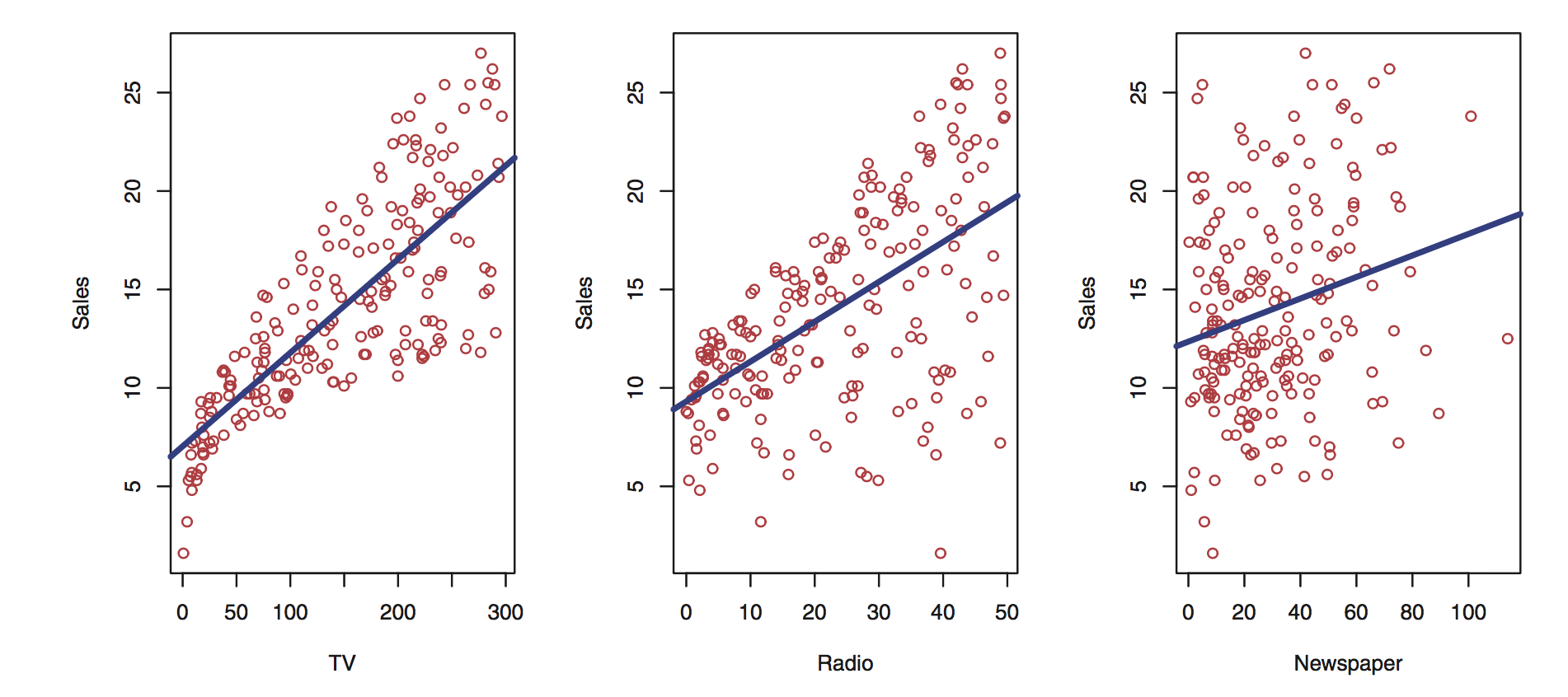

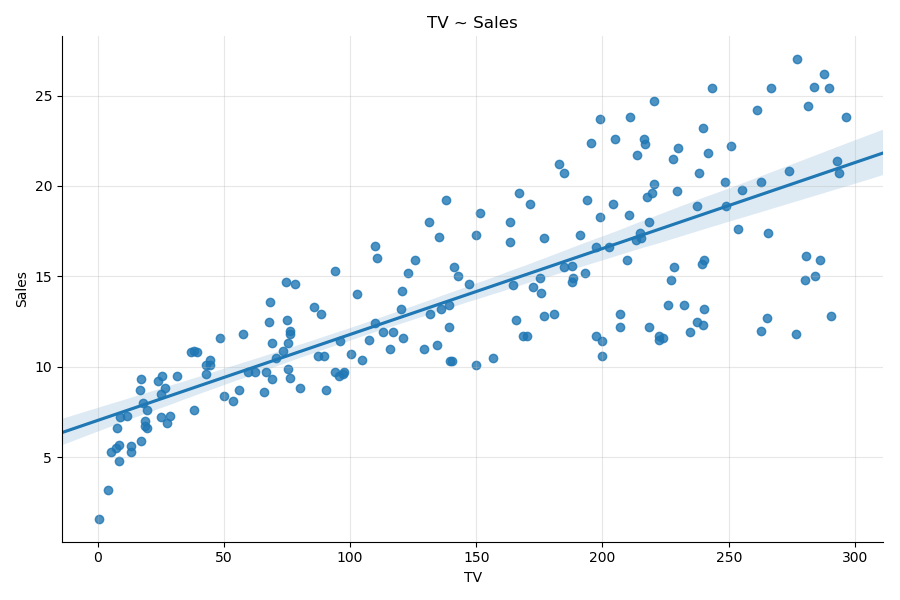

Start by plotting each input variable to the outcome variable.

You can already infer some information from these plots:

As TV and radio spending increase, so do sales.

Newspaper spending impact on sales is less pronounced, although there is a trend.

It looks like TV spending is more efficient than radio as the overall trend of the plot is steeper.

Calculating the correlation between the variables gives:

df = pd.read_csv('advertising.csv')

df.corr()['Sales']

TV 0.782224

Radio 0.576223

Newspaper 0.228299

Sales 1.000000Which confirms what we inferred from the plots above.

Univariate Linear regression

As mentioned above, univariate linear regression is when you want to predict the values of one variable from the values of another. Let's start by building a linear model between sales and TV, which is the variable most correlated with the outcome.

We want to find the best coefficients a and b such that:

For that, we turn to the statsmodel library in Python, which can be installed with:

pip install statsmodels

or

conda install statsmodels

What is exog and endog?

If you look at the statsmodel documentation on OLS, you will notice that the input variable is called exog, while the outcome variable is called endog. These are shorthand for:

Endogenous: caused by factors within the system.

Exogenous: caused by factors outside the system.

How this relates to the concept of predictors and target variables is fully explained here. In our case, we will continue to use terms like input, dependent, or predictor variable for X, and output, outcome, target, or independent variable for y.

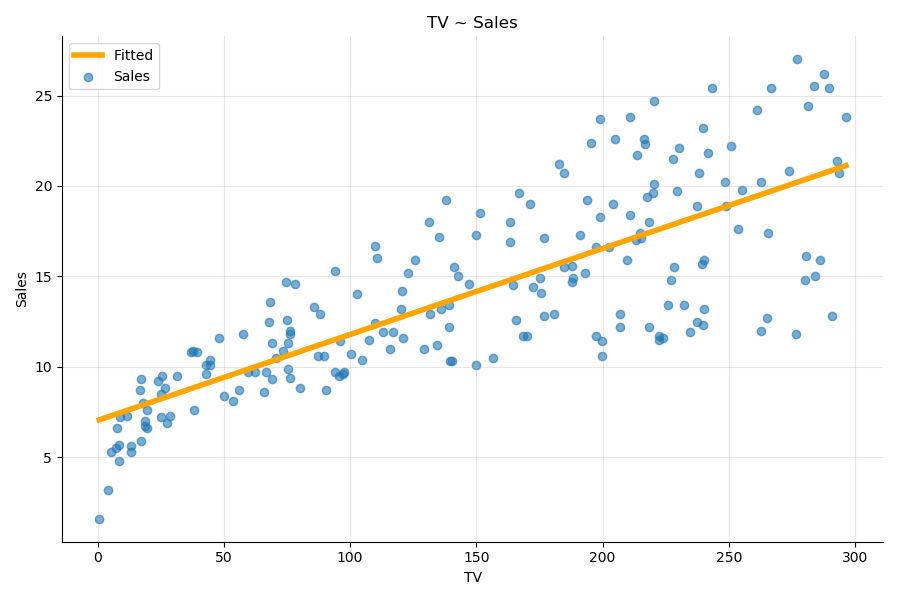

Sales ~ TV

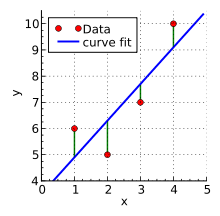

To build a linear model between sales and TV, use the method called ordinary least square, or OLS. In short, the OLS method will find the line closest to all the points of the plot as shown:

We will come back to the inner workings of the OLS method later on.

The following is the code to build and fit the linear regression model to the data:

# import the modules

import statsmodels.api as sm

import pandas as pd

# Load the dataset

df = pd.read_csv('advertising.csv')

# single out the input variables X

X = df['TV']

# Add a constant

X = sm.add_constant(X)

# define the target variable y

y = df['Sales']

# Define the model

model = sm.OLS(y, X)

# Fit the model to the data

results = model.fit()

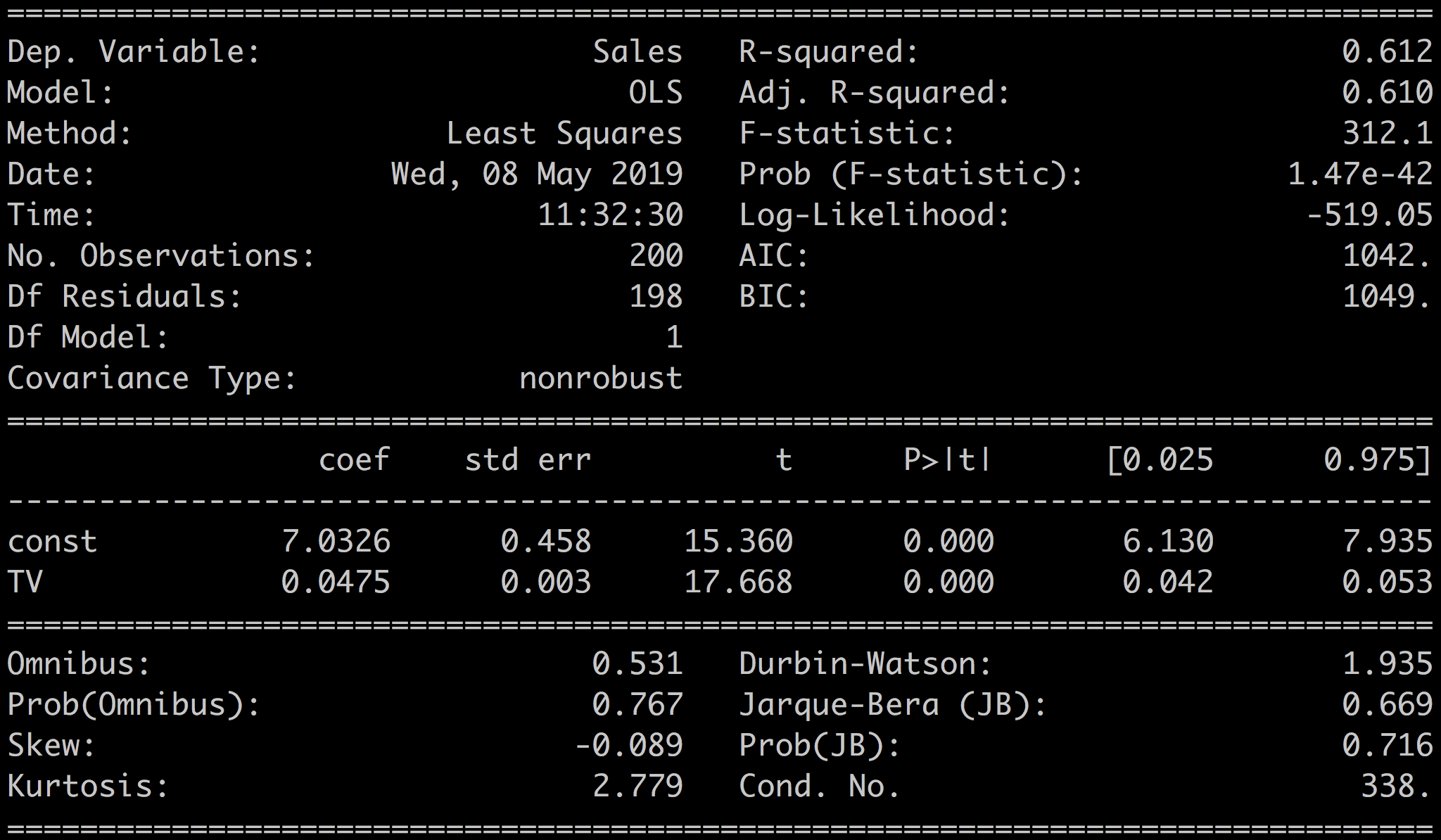

print(results.summary())Which gives the following output:

Let's break this down. For a start, we will only focus on a few of the metrics in this chapter. The rest we will save for later.

The most important element of the results is the line with the values for the coefficients, p-value, and confidence intervals:

The metric R-squared:

Code Review

But first, let's go over the code above and explain what we did. Two things need our attention: formatting the input variables into X, and fitting the model.

We first select the predictor variable, in our case TV:

X = df['TV']X is an array of 200 samples x = [x_1, x_2, ... , x_N]^T. If you feed that vector to the OLS method, it will try to find the best line that corresponds to:

This line goes through the origin point and does not have a constant term. However, you want to find the best line, the best parameters a and b, that fits:

For that, you need to add a constant vector to df['TV'] so that X becomes an array of dimension 2,N:

X = [[1,x_1],

[1,x_2],

...

[1,x_N]]Use the add_constant method in statsmodel:

X = sm.add_constant(X)If you visualize the shape and head of X before and after, you get:

X = df['TV']

print("before: X shape: {}".format(X.shape))

> before: X shape: (200,)

X = sm.add_constant(X)

print("after: X shape: {}".format(X.shape))

> after: X shape: (200,2)A const column has been added to X. Next, define a simple OLS model based on that data:

model = sm.OLS(y, X)And call the fit() method to fit the model to the data:

results = model.fit()Finally, print the summary of the results with print(results.summary()).

Interpreting the Results

The upper-left quadrant of the results are mostly a summary of the method indicating the name of the outcome variable (here, Dep. Variable ), which is sales; the model, OLS; the method, least squares; and the number of samples (here, No. Observations), 200.

Before we look more closely at the numerical results, we can plot the line estimated by the OLS method with the results.fittedvalues method. As its name indicates, the fitted values can be obtained from the regression coefficients:

results.fittedvalues = results.params['TV'] * df['TV'] + results.params['const']You can also access the residuals, i.e., the error between the real values and the fitted values.

results.resid = df['Sales'] - results.fittedvaluesFor ease of manipulation, let's add the fitted values to the initial DataFrame.

df['fitted'] = results.fittedvaluesTo plot the fitted values versus the real values, sort the DataFrame. This is just for plotting convenience.

df.sort_values(by = 'TV', ascending = True, inplace = True)Then plot the fitted values and the residuals with:

plt.scatter(df.TV, df.Sales, label = 'Sales' )

plt.plot(df.TV, df.fitted, label = 'Fitted' )

plt.legend()

Coefficients

Let's focus on the coefficients and related statistics:

The coef is the coefficient value in the equation:

In our case, we have:

P-values

Next, the P>|t| value is the p-value associated with the coefficient. The p-value for each coefficient tests the null hypothesis that the coefficient is equal to zero (no effect). The full values of the p-values can be obtained with:

print(results.pvalues)

const 1.406300e-35

TV 1.467390e-42You can see here that the p-values are well below the standard threshold of 0.05. You can, therefore, reject the null hypothesis and conclude that the coefficient values are relevant given the data.

T-Statistic and Standard Error

The standard error is an estimate of the variations of the coefficient.

The t-statistic is the coefficient divided by its standard error.

The t-statistic is a measure of the precision with which the regression coefficient is measured. A coefficient with a comparatively small standard error, is more reliable than one with a comparatively large standard error.

In our case, looking at the coefficient for TV (a = 0.0475), we have a standard error of 0.003, which is much lower than the coefficient, and a t-value of 17.67, which is much higher than the coefficient.

Confidence Intervals

The 97.5% confidence interval (CI) is the likely range of the true coefficient. The confidence interval reflects the amount of random error in the sample and provides a range of values that are likely to include the unknown parameter.

R-Squared

R-squared, also known as the coefficient of determination, measures the predictive quality of your model. R-squared is defined as the amount of variation of the target variable which is explained by your model.

R-squared is always positive and lower than 1.

R-squared is helpful when comparing different models. In the following demo, we'll build models based on the other two media; radio and newspaper and compare the coefficients and R-squared values for all the media.

R-squared is calculated as the ratio of the variance of the target variable with the variance of the residuals:

with

The residual sum of squares:

The total sum of squares

The fitted values

And the mean of the observed data

Summary

Looking at the results of a linear regression, these are the main things you need to look at to assess the quality of your model:

The coefficients are an indication of the correlation of your input variable(s) with the outcome.

The associated p-values and confidence intervals tell you how much trust you can put in these coefficient estimations. The p-value also tells you how confident you can be that each individual variable has some correlation with the outcome.

When the p-value > 0.05, or when the confidence interval contains 0, then the coefficients are not reliable.

The t and standard error also give an indication of how much the coefficient varies around the estimated value. You want a high t and a low standard error compared to the value of the coefficient.

The R-squared shows you how much of the variations in the target variable are explained by the model. The higher the better. The R-squared is particularly relevant when using the model to make predictions.

But, wait! What about the other predictors radio and newspaper?

Check out this screencast where I take you through how to build the following two other univariate models:

Sales ~ Radio

Sales ~ Newspaper

We compare these models with the Sales ~ TV model and identify the best model based on the metrics we've seen in this chapter.